The Missing Ritual: What Mexico’s Fintech Export Story Leaves Out

Everyone says Mexican fintechs are “born global.” This ethnographic audit treats that claim like a crime scene, tracing what is actually being exported from Mexico to the Global South—and what critical social value disappears along the way.

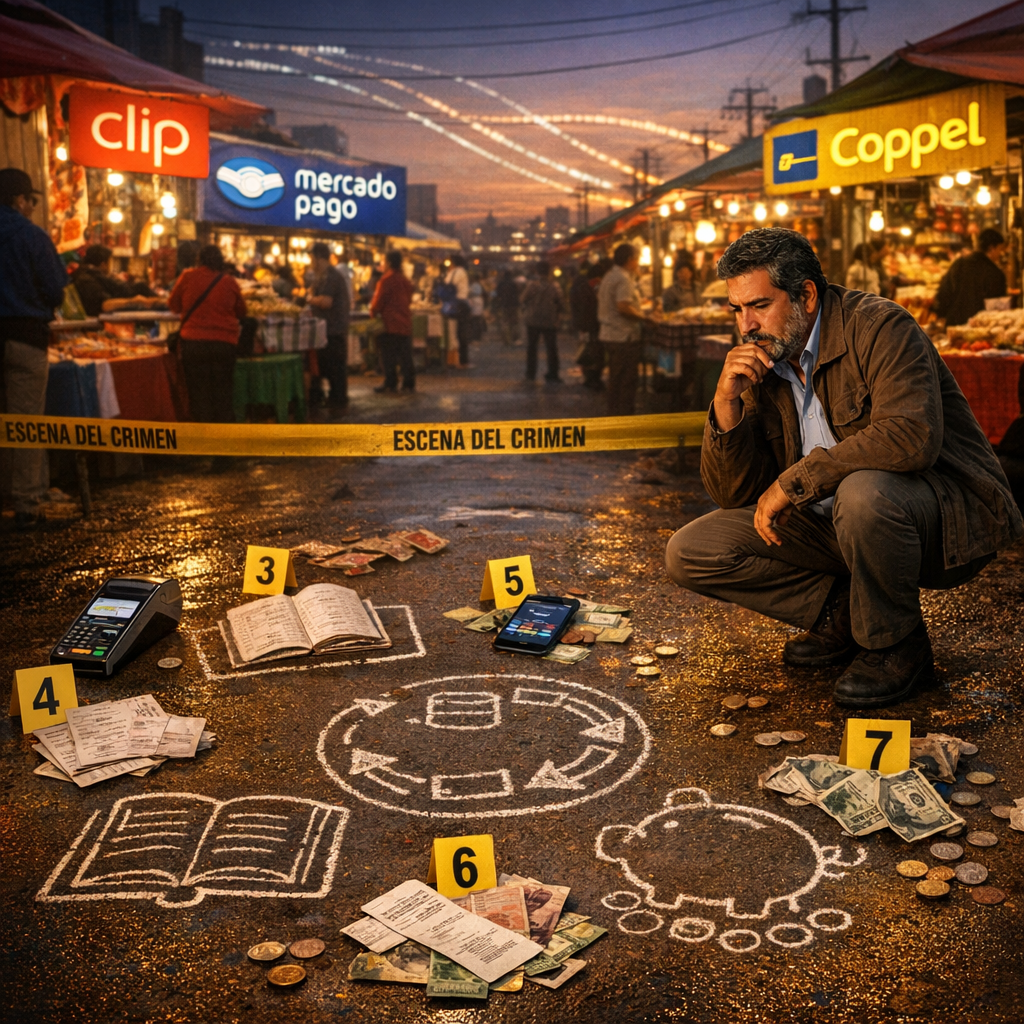

The Hook: Scene at a Borderless Crime Scene

The WhatsApp call crackles to life in a cramped tienda in Puebla and a crowded bodega in Lima at the same time.

In Puebla, Lucía wipes her hands on her apron before tapping a lime‑green payment link a supplier has just sent her. In Lima, Carlos does the same. They have never met, yet their thumbs follow the same choreography: open WhatsApp, tap link, confirm tiny charge, trust a logo they did not grow up with.

On both screens, the interface looks eerily identical: the same minimalist card illustration, the same reassuring copy in neutral Spanish, the same three‑step progress bar. Somewhere far from both counters—on servers engineered in Mexico City, investor decks reviewed in San Francisco, and regulatory templates copied into a drive folder—logic written for Mexican constraints is now running their lives.

If this were a crime scene, the first thing an anthropologist would notice is not the app itself but the ritual it has replaced.

Lucía used to keep a paper notebook with names and debts. Carlos did too. Those ledgers anchored a web of trust: neighbors vouching for each other, gossip enforcing repayment, shared shame limiting default. Now a Mexican‑built underwriting engine quietly decides who is trustworthy—and it exports that decision logic thousands of kilometers away.

Everyone in the industry repeats a triumphant line: if it works in Mexico, it can work anywhere.

This report asks a less comfortable question: when Mexico’s fintech rituals travel, what gets lost at the border?

I will treat Mexico’s fintech export story as an open case file. The obvious evidence is celebrated: unbanked markets served, cross‑border expansion, capital attracted. But like any good forensic audit, we will look for what is missing: the unrecorded rituals, the muted voices, the unpriced risks.

The Genesis: How Mexico Turned Constraints into a Badge of Honor

Every tribe tells a founding myth. In Mexican fintech circles, it begins with scarcity.

Roughly 36% of Mexican adults remain unbanked and another 20% are underbanked. More than 90% of transactions still happen in cash. About 30% of GDP flows through informal channels. Yet over 80% of people carry smartphones in their pockets.

This is the paradox that founders like to celebrate: high connectivity, low formal finance.

Then there is the annual remittance ritual. More than $50 billion flows from migrants back to Mexico each year—money that often lands in cash, at counters staffed by people who know clients by name but not by credit score.

In 2018, the state stepped into this charged terrain with the Fintech Law, a regulatory experiment meant to host innovation without letting it run feral. Officially, this law established categories for electronic payment institutions, crowdfunding platforms, and virtual assets. Unofficially, it signaled that the tribe had the state’s implicit blessing to experiment—within limits.

Pressed between exclusion and opportunity, founders began building.

- Clip armed small merchants with mobile card readers so they could finally accept plastic in a cash‑heavy economy.

- Konfío and its SME peers stared at the gaping hole where business credit should be and tried to fill it with alternative data.

- Klar and albo framed themselves less as banks and more as clean, mobile‑first companions in a country where branches and opaque fees had long eroded trust.

- Kueski peered into micro‑needs—small, urgent loans—and tried to rewire them via data and instant decisions.

- Bitso spotted a border ritual—remittances—and used crypto rails to make that rite cheaper and faster.

It is tempting to render this as a linear progression: constraint → ingenuity → product → scale.

But an anthropological reading sees something else: a new tribe forming around a shared identity—those who can turn Mexican chaos into exportable order. The informal economy becomes not just a market problem but a proving ground. Connectivity gaps and fraud risks, once seen as obstacles, are recast as badges: if your system survives here, it deserves to travel.

This is the origin story fueling today’s expansion. And it hides a quiet assumption we will keep examining: that complexity faced at home automatically confers moral and technical authority abroad.

The Invisible Conflict: Whose Rituals Get to Define “Good Finance”?

On pitch decks, Mexico appears as a laboratory that simulates the Global South—a controlled environment where products can be stress‑tested before being exported.

On the ground, the picture is messier.

Founders argue that constraints are their competitive edge:

- intermittent connectivity forces them to design offline‑capable apps;

- low trust in banks leads to hyper‑simple UX and friendly, WhatsApp‑native onboarding;

- high fraud risk turns them into experts in defensive design;

- regulatory complexity under the Fintech Law forces compliance to be built into the core.

From there, a tidy argument follows: if these systems work amid Mexico’s volatility, they will travel well to Lima, Bogotá, Lagos, Nairobi.

The conflict sits elsewhere.

Technically, much of this is true. Socially, each market already has its own financial rituals—how debt is requested, how shame is distributed, who vouches for whom, how risk is forgiven or punished. When Mexican fintech models cross borders, they do not enter empty land. They arrive as a new tribal code, layered on top of existing customs.

The invisible conflict is not about expansion per se; it is about whose logic becomes dominant:

- Does a Mexican‑built credit model, trained on Mexican behavioral proxies, get to define who is creditworthy in Peru or Colombia?

- Does a UX born from distrust in Mexican banks map cleanly onto places where banks may be disliked for different reasons—or where informal savings circles carry more symbolic weight than any bank?

- Do Mexico’s regulatory habits, shaped under a specific Fintech Law, become the silent template for other central banks even when their societies tolerate risk differently?

This conflict is rarely named because the export story often travels with a moral halo: these tools include the excluded, modernize economies, formalize chaos.

An anthropologist would phrase it differently: a dominant tribe is projecting its rituals outward and calling the result “neutral infrastructure.”

Evidence & Insights: The Case File of Mexico’s Traveling Fintechs

Instead of a celebratory catalog, consider this a set of annotated exhibits.

Exhibit A: Clip and the Card Ritual

Clip began in 2012 with a straightforward intervention: give small merchants a mobile point‑of‑sale (mPOS) device so they could accept cards.

In a terrain where over 90% of transactions were cash, Clip’s bright card readers became new ritual objects on market tables. They were less about hardware and more about symbolism: I am part of the formal grid now. I can take plastic.

When Clip extended its reach into countries like Argentina and Colombia, the company found an oddly familiar scene: high informality, cash dependency, merchants locked out of card networks. The product required minimal adaptation—logos and support scripts tuned to dialect, pricing and regulatory filings adjusted to local rules—but the core script stayed the same.

The hidden shift was anthropological. Where merchants once mediated trust face‑to‑face, Clip’s devices began mediating it through networks and acquirers. The company exported not only a device but a re‑coding of what counts as a “real” payment.

Exhibit B: Konfío and the SME Credit File

Konfío, founded in 2013, set out to provide unsecured working capital loans to SMEs. Traditional banks either ignored these businesses or smothered them in paperwork. Konfío looked at digital traces instead: invoices, bank feeds, payment histories, alternative signals.

As it extended its technology into markets like Colombia, it discovered that SME precarity has a shared pattern: irregular cash flows, informal bookkeeping, tax ambiguity. Konfío’s data‑driven models traveled with minor tuning.

Here, the invisible leap was more subtle: an algorithm trained on Mexican firms decided that a Colombian shop with similar numbers was “the same kind of risk.” Anthropologically, a classification system born in one tribe was being used to sort another.

Exhibit C: Klar, Kueski, and the Individual as Data Pattern

Klar, launched in 2019, positioned itself as a mobile banking platform for Mexico’s underbanked: no hidden fees, transparent terms, app‑first logic.

Kueski, dating back to 2012, offered microloans based on alternative data.

Both share a faith in data that can stand in for reputation.

When their approaches—or derivatives of them—move into Peru, Brazil, or neighboring countries, the codebase does much of the work. Behavioral features are mapped; repayment curves are compared. The models assume that late‑night phone usage, spending patterns, or utility payment history mean roughly similar things across borders.

Sometimes they do. Sometimes they don’t.

This is the quiet risk: the more these systems spread, the more human beings in very different cultural worlds are turned into datapoints inside an inherited Mexican grammar of risk.

Exhibit D: Bitso and the Rewiring of Remittances

Bitso emerged in 2014 with a bold proposition: use crypto to move value cheaply from the U.S. to Mexico, where remittances exceed $50 billion a year.

The company later expanded into Argentina and Brazil, carrying with it a conviction that border money flows can be re‑architected through digital assets.

Technically, the model required limited alteration. Remittances and cross‑border flows in Latin America share structural similarities: migrants abroad, families at home, high fees, inconvenient pickup.

Socially, though, the ritual of receiving money varies. In some places the physical collection—the bus ride to town, the conversation at the counter—is a significant social moment. Digitizing that transfer doesn’t just cut costs; it collapses a ritual.

Bitso exports efficiency. It also exports silence where there used to be small talk, waiting rooms, and very human forms of verification.

Table 1: The Winners vs. Losers Scorecard (Preliminary)

| Stakeholder | Short‑Term Gains | Long‑Term Risks or Losses |

|---|---|---|

| Mexican fintech founders | New markets, valuation growth, credibility | Overconfidence in homegrown models; blind spots abroad |

| Global investors | Access to scalable, constraint‑hardened platforms | Herding around copy‑paste theses, missing local nuance |

| Foreign regulators | Ready‑made templates, faster innovation | Imported practices that may not fit local social norms |

| Local informal lenders | None; often displaced | Loss of livelihood; erosion of community‑based safety nets |

| End users (borrowers, SMEs) | Faster access, more options, sometimes cheaper | Datafied reputations, opaque exclusion when models misread |

Designed for Constraints: The Tribal Code Behind the Interfaces

Constraint is often described in engineering terms: spotty connectivity, low trust, fraud risk, regulatory friction.

In Mexico, constraint is also social.

- Many people still prefer cash, partly due to low financial literacy and a lived memory of banking failures.

- Informal savings circles, family loans, and notebooks of store credit are not inefficiencies but social glue.

- Merchants use cash to manage identity and obligations as much as to run a business.

Mexican fintechs learned to survive in this environment by writing a specific tribal code.

Product Design as Ritual Engineering

Apps are:

- Offline‑capable, because connections fail during the very hours people need to transact.

- Radically simple, because interface confusion is interpreted as disrespect, not just inconvenience.

- WhatsApp‑native, because that is where social life already happens—and where trust still resides.

- Agent‑backed, because in many neighborhoods it is easier to believe a cousin’s friend with a branded T‑shirt than a disembodied app store description.

When this code travels to other Global South markets, it often fits surprisingly well. Intermittent connectivity, limited trust, and the centrality of a messaging app are widespread.

Yet exporting this design language also exports an implicit theory of the user: a cautious, partially connected, distrustful person who must be coaxed gradually into formal systems. That archetype may obscure other local identities—users who distrust for different reasons, or who organize their finances along clan, caste, or cooperative lines.

Risk Models as Cultural Hypotheses

Alternative data models—Konfío’s SME scores, Kueski’s consumer profiles, Klar’s behavioral signals—are often described as if they were purely mathematical.

But every input is a cultural hypothesis.

- Paying a phone bill on time is taken as a proxy for reliability.

- Transaction regularity stands in for stability.

- Certain merchants, locations, or purchase patterns are coded as high or low risk.

These hypotheses are trained in Mexico’s specific mix of formality, informality, and digital behavior. When the same models, or their derivatives, are dropped into Peru or Colombia with “minimal adaptation,” the underlying bet is that the same proxies signal the same virtues.

Sometimes that holds. But when it doesn’t, the result is not just model error; it is misrecognition. People are misread according to somebody else’s ritual.

Compliance‑Built Architectures as Ideological Export

Mexico’s 2018 Fintech Law forced startups to take regulation seriously at the architectural level. Systems were built with audit trails, identity verification layers, and change logs meant to satisfy a skeptical state.

These compliance‑ready designs are now part of the export package:

- codebases that make KYC layers easy to adapt per country;

- reporting modules that speak in a language regulators can accept;

- templated ways of engaging central banks, honed through trial.

Other countries, lacking their own mature fintech frameworks, often look to Mexico’s experience as a blueprint.

Anthropologically, this is a significant shift: a regulatory culture born from Mexican political history starts to shape what other states view as reasonable oversight.

The New Export: Playbooks, Not Just Products

Hardware and code are the visible artifacts. The real exports are playbooks.

Operational Rites: Agents, Retailers, and Embedded Channels

Mexican fintechs have scripted a set of operational rituals that now travel:

- Agent networks: local “ambassadors” who do onboarding, cash‑in/cash‑out, light support. These networks translate abstract apps into human faces.

- Retail partnerships: alliances with chains and corner stores that turn checkouts into financial hubs.

- Embedded finance: credit lines and payment options woven into marketplaces and SaaS tools.

When these scripts appear in other Latin American markets, they often arrive with Mexican fingerprints all over them: training modules translated, incentive schemes reproduced, field management practices cloned.

Data Models and Underwriting Frameworks

Konfío‑like approaches to SME underwriting, Kueski‑style micro‑loan assessment, and Klar’s digital spending insights are increasingly treated as exportable assets in their own right.

Some Mexican platforms already:

- license risk engines to banks and startups abroad;

- white‑label infrastructure so a local brand can operate on Mexican‑built rails;

- offer consulting to help foreign institutions “get comfortable” with alternative data.

In these arrangements, the logic of risk—shaped in Mexico’s tension between informality and aspiration—becomes a standardized product.

Regulatory Templates and Cross‑Pollination of Founders

Beyond code, there is regulatory choreography:

- step‑by‑step guidelines on how to present a product to a wary central bank;

- draft policies on safeguarding customer funds;

- playbooks for participating in or lobbying for regulatory sandboxes.

Mexican founders and operators increasingly advise or co‑found startups in Colombia, Peru, and occasionally beyond Latin America, bringing these rituals with them.

The story is usually told as capacity‑building. Another reading is that a particular priesthood of compliance—shaped in Mexico—now tours the region preaching a specific gospel of “responsible innovation.”

Table 2: The Traveling Playbook Kit

| Component | Origin in Mexican Practice | How It Travels |

|---|---|---|

| Agent onboarding rituals | Cash‑in/cash‑out networks serving informal areas | Replicated in new markets with local hires, same scripts |

| Risk scoring frameworks | Alt‑data for SMEs and consumers (Konfío, Kueski) | Licensed or cloned with light re‑weighting |

| Regulatory engagement templates | Negotiated under 2018 Fintech Law | Adopted as de facto proposal for other regulators |

| WhatsApp‑centric UX patterns | Built where WhatsApp is de facto infrastructure | Copied into regions where messaging apps rule |

| White‑label fintech stacks | Klar‑, albo‑, Bitso‑style infrastructure | Used by banks/startups to shortcut years of build |

Mexico as a Hub: The City Where Codes Converge

Walk through certain districts of Mexico City today and you can feel the density: clusters of engineers, risk analysts, product managers in cafés, talking not about “Latin America” in the abstract but about very concrete questions like: Which Peruvian data source best mirrors SAT filings? How do we route around a Colombian ID quirk without rewriting the stack?

The city has become a magnet for several reasons:

- Talent density: a decade of building in adverse conditions has produced specialists in emerging‑market fintech design, risk, and operations.

- Capital flows: in 2024, Mexico’s fintech sector drew over $865 million across 50 deals, much of it from U.S. investors who increasingly view Mexico as a launchpad for wider Global South bets.

- Ecosystem integration: collaborations between fintechs and banks—fostered in part by global partners like Galileo—have turned the city into a site where formal and informal, old and new, intersect.

Investors do not just bring money. They bring a worldview: Mexico as prototype factory. Clara’s $80 million round, backed by names like Acrew, Citi Ventures, Coatue, DST Global, Kaszek, Monashees, and General Catalyst’s Customer Value Fund, was explicitly about using Mexican‑hardened models to scale across Brazil, Mexico, and Colombia.

When compared with São Paulo, Bogotá, or Buenos Aires, Mexico’s edge is not size alone; Brazil’s market is larger, São Paulo’s tech scene older. Mexico’s advantage is narrative: a place that is chaotic enough to be “real,” yet regulated enough—via the Fintech Law and emerging sandboxes—to reassure global capital.

Founders from neighboring countries are relocating to Mexico City not simply for money but to inherit this double legitimacy: “we know chaos; we know regulators.”

Once again, a new tribal center is forming.

Challenges, Limits, and the Cases That Don’t Fit

Every forensic audit pays attention to the anomalies—the expansions that falter, the models that misfire, the regulations that push back.

Regulatory Friction and Uncertainty

While Mexico’s Fintech Law created a known environment at home, foreign markets often present a jagged terrain:

- Some lack dedicated fintech laws, forcing startups into gray zones.

- Others change rules rapidly, creating planning uncertainty.

- Data protection regimes vary widely, making cross‑border data flows risky.

For Mexican companies accustomed to building compliance into their architectures, this can be a double‑edged sword: they arrive “over‑structured” for a market without such expectations, or under‑prepared for suddenly strict regimes.

Infrastructure That Refuses to Globalize

Not all rails are portable.

Real‑time payment systems like Mexico’s CoDi, whose growth has been buoyed by high internet and mobile usage—over 100 million Mexicans online and 123.5 million mobile connections—create expectations about how quickly and cheaply money should move.

When a Mexican fintech steps into a market whose payment rails are slower or more fragmented, it faces a painful choice: lower standards or build expensive workarounds.

Some of the most touted “global” stacks are quietly more local than they admit, stitched to Mexican ID systems, payment schemes, and legal idiosyncrasies.

Cultural Misreads and Product Rejections

Behavioral nuances travel poorly.

In Mexico, a historical distrust of banks and a shift toward digital payments—cash in stores down 23% in a year, contactless credit card use rising from 1% to 5.1%—create a specific arc of adoption. People may dislike banks but increasingly like the convenience of phone‑based payments.

In another market, people may trust banks more but resent foreign apps. Or they may rely heavily on community savings groups in ways that make individualized credit apps feel alien.

At least one Mexican fintech that tried to expand its credit product abroad discovered that default curves looked too different—even after controlling for economics. The model, confident in Mexican proxies, misread repayment signals in the new country. Local users found the pricing punitive and the UX paternalistic. The company quietly pulled back, reframing the attempt as “strategic refocus.”

From a social angle, what happened was simple: a foreign tribal code failed to gain legitimacy.

The Missed Opportunity: Listening Before Exporting

The largest gap in many expansion stories is not technology but ethnography.

Mexican teams, confident in their constraint‑tested designs, often underinvest in understanding:

- local debt rituals;

- informal mediators of trust;

- gendered patterns of financial control;

- how shame and honor shape default.

By treating new markets as scaled versions of Mexico, they miss chances to co‑create products with local communities, rather than imposing templates.

The Strategic Shift: From Exporting Answers to Exporting Questions

If Mexico truly wants to be a hub for the Global South, it must change what it exports.

For Founders: Reframe Constraint as a Shared Question, Not a Solved Problem

Building in Mexico does give companies real advantages: hardened infrastructure, intuition for fraud, skill with alternative data.

But the next wave of global players will be those who treat these as hypotheses to be tested—with local communities, not on them.

Actionable shifts:

- Ethnographic fieldwork as a core function: embed researchers, not just sales teams, in new markets before shipping models. Map local financial rituals with the same rigor used for metrics.

- Configurable tribal codes: design products so that key rituals—how credit is requested, how default is handled, how shame is mitigated—can be altered meaningfully, not just cosmetically.

- Local risk councils: form advisory groups of local lenders, community leaders, and users to review and contest risk proxies before go‑live.

For Policymakers: Sandboxes That Ask “Whose Logic Is This?”

Regulators in other emerging markets often admire Mexico’s Fintech Law and sandbox experiments.

The strategic shift is to treat imported playbooks as starting points, not standards.

Actionable shifts:

- Context‑first guidelines: when a Mexican fintech applies to operate, ask explicitly how its models adapt to local debt culture, not just to local law.

- Public ethnographic reports: require impact assessments that describe the social changes a product may trigger—loss of local lenders, changes in household bargaining power—not only financial outcomes.

- Reciprocity clauses: if Mexican regulatory templates are used, create channels for local insights to flow back, influencing the next iteration of those templates.

For Investors: Fund the Cost of Slower, Deeper Adaptation

Capital today often rewards fast copying: if Clip worked in Mexico and Colombia, find “the Clip of X.” If Bitso cracked remittances, back more crypto‑rail propositions.

A different strategy is available.

Actionable shifts:

- Back ethnographic moats: treat genuine, on‑the‑ground cultural understanding as a defensible asset worth funding.

- Design metrics for social fit: beyond MAUs and NPLs, ask how many local partners co‑designed features, how many product decisions changed after user ethnography.

- Value multi‑hub models: invest in companies building shared infrastructure across hubs—Mexico City, São Paulo, Bogotá—rather than expecting one city’s logic to dominate.

The Big Picture: Mexico as a Mirror, Not a Master

The standard story says: Mexican fintech startups, forged in a hard market of cash, informality, and distrust, are now reshaping global financial services from the bottom up. They export product models, tech, and playbooks to underserved markets that look just enough like home.

That story is not wrong. It is simply incomplete.

From an anthropologist’s vantage point, Mexico is less a universal laboratory and more a mirror. The constraints it has forced its startups to face—gaps in credit, dependence on cash, fragmented regulation, behavioral mistrust—are real but also deeply Mexican. When its fintechs cross borders, they carry that specificity with them.

The crime scene question is this: as these tools spread, what social value goes missing?

- Some informal lenders and local credit circles lose their place in the economy before formal alternatives have learned how to carry the same relational weight.

- Some regulators inherit practices that may be too strict or too lenient for their own social fabric, simply because “it worked in Mexico.”

- Some users are converted from neighbors with names into datapoints that match or mismatch a model trained elsewhere.

The next decade will likely see Mexican‑born players pushing harder into SME credit, cross‑border payments, embedded finance, and crypto/remittances. The raw ingredients are there: constraint‑tested architectures, mobile‑first societies, investors aligned around a Global South thesis.

But the real frontier is not whether Mexican products can scale. It is whether Mexican founders, regulators, and investors choose to export questions as eagerly as they export code.

Questions like:

- What kinds of trust are we displacing when we bring formal finance into informal worlds?

- How do we design models that can be challenged—and altered—by the communities they score?

- When we win the efficiency battle, what quiet rituals do we lose, and which of them were holding people together?

If Mexico can become the hub that keeps asking those questions aloud, then its fintech expansion will be more than a commercial success. It will be a rare experiment in global finance that takes the social fabric seriously.

And the crime scene tape that now rings our financial rituals might be replaced by something more subtle: a shared awareness that every export carries a hidden cost—and a shared choice to reckon with it.

References

- Mexico’s unbanked and underbanked population, cash usage, informality, and remittance figures drawn from research context provided in prompt.

- Smartphone penetration and digital connectivity statistics for Mexico (over 80% smartphone ownership; 100M+ online; 123.5M mobile connections) based on research context citing PYMNTS and related sources.

- Description of Mexico’s 2018 Fintech Law and its role in shaping regulatory frameworks informed by research context referencing msblabs.org and mexicohistorico.com.

- Data on adoption of CoDi, shifts in cash usage, contactless card use, and consumer behavior in Mexico grounded in research context citing pymnts.com, thunes.com, and moldstud.com.

- Funding statistics for Mexican fintech in 2024 ($865M across 50 deals) and international investor participation sourced from research context citing agilitypr.news.

- Example of Clara’s funding round (US$80M led by international investors including Acrew, Citi Ventures, Coatue, DST Global, Kaszek, Monashees, and General Catalyst’s Customer Value Fund) from research context citing LinkedIn and FasterCapital.

- Observations on regulatory challenges, compliance costs, and strategies for navigating diverse regimes based on research context citing msblabs.org, techcrunch.com, fastercapital.com, yativo.com, and mexicohistorico.com.

- Narrative descriptions of Clip, Konfío, Klar, Kueski, Bitso, and other Mexican fintechs’ business models and expansion patterns grounded in the factual summaries included within the research context.

Related Articles

Who Stole the Value? A Forensic Audit of Giants, Startups, and the Customer Left Out of the Deal

Treating today’s innovation economy as a crime scene, this essay investigates what quietly disappears when incumbents and startups reshape finance, health, retail, mobility, education, and climate tech. Beyond pitch decks and marble lobbies, who actually captures the value—and at what human cost?

The Year We Misread the Checkbox: How a Single UX Choice Rewired Giants and Startups

Writing from 2050, a radical futurist looks back on 2024 and argues that the true battle between traditional industries and startups in banking, retail, health, and mobility never took place in boardrooms or pitch decks, but inside a single, tiny UX artifact: the checkbox. By following that microscopic element, this manifesto rewrites the history of incumbents vs. startups as a struggle over who controls consent, data, and time.

The scene of the silent crime: where has courage been lost between giants and startups?

A monk‑analyst steps onto the “crime scene” of the digital economy—financial services, retail, healthcare, mobility, education, and manufacturing—to investigate a silent disappearance: the deeper value that customers, workers, and communities expected from the transformation between traditional industry and the startup ecosystem.